Foreword

The Monthly Update from Trajectory: March 2026

A New Low

There’s no easy way of putting this; we are now more pessimistic than at any point in the last two years.

We are not looking on the bright side of life. The pint glass is half empty. Lady Luck is out of the office for the foreseeable.

The Optimism Index nudged down again in February and is now trawling the slough of despond. Underneath that attention-grabbing headline are a number of moving parts. Optimism among the majority stayed much the same in February - the overall number was brought down by previously tiggerish groups (including men, Millennials and Londoners) losing their bounce. The polarisation between genders and generations that we’ve noticed in recent months is declining as sentiment converges on the shady side of the street.

I’m afraid that the bad news doesn’t stop there. Confidence in both household finances and in the performance of the UK economy dropped sharply despite stable inflation and interest rates. This has fed through to spending expectations - especially on big ticket items - which have retracted like a snail into a shell. Looking through the data, there is a discernable nervousness among consumers. There’s been an increase in the number of people agreeing that they have less disposable income than they did a year ago and half the population are worried about paying regular household bills. Consumers are twitchy.

The fieldwork was conducted in early February, well before the new war in the Middle East but at the height of news coverage of the Epstein files. While our 1,500 respondents were answering our questions, the police launched an investigation into Peter Mandelson’s alleged misconduct in office and the Prime Minister’s Chief of Staff, Morgan McSweeney, resigned. (Despite being deceased these last seven years, Jeffrey Epstein still has a surprising amount of influence.) Predictably, trust in politicians dipped last month. Trust in business leaders was also down.

The full and nourishing detail of the Optimism Index is available to subscribers. Details at the bottom of this missive.

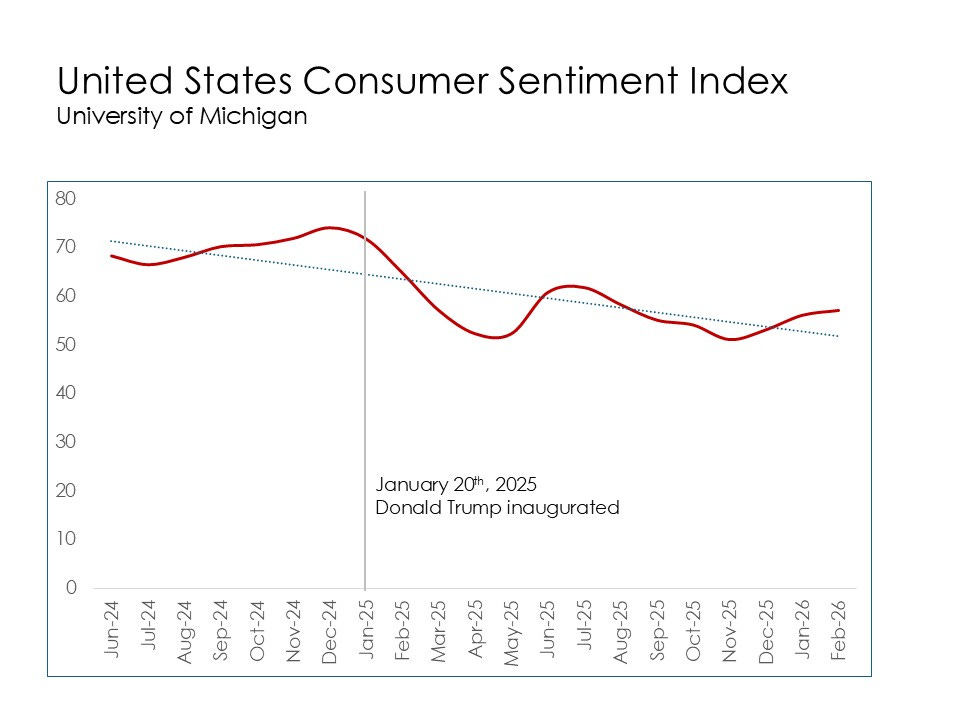

Meanwhile, Stateside…

While British consumers lost confidence in their own finances and in the British economy last month, American consumers were more phlegmatic.

The University of Michigan sentiment index measures how Americans feel about their own finances and the American economy generally. As with any average figure, a lot of nuance is concealed beneath the headline. The overall number was held up by wealthier, college-educated Americans - often those holding stocks. Sentiment among Americans with lower incomes and without investment portfolios declined.

Sustainable Interest?

Is our collective interest in sustainability … sustainable?

The political will to live in a more sustainable way seems to have faltered. The United States has withdrawn from the Paris Climate Agreement and the UN Framework Convention on Climate Change. In the UK, the Greens scored a notable by-election victory last month and in terms of voting intention they are tied with Labour on 16% in Politico’s Poll of Polls. However, the Green Party have reframed their offer to the electorate; they talk more about social justice and overseas wars and less about the environment. They are now much less likely to be portrayed as Birkenstocks-and-socks tree-huggers. Meanwhile, the Conservative Party insist that the Net Zero target can’t be achieved while Reform would abandon the target altogether. In Europe, there is some backsliding on environmental regulation. The recent COP conferences feel less consequential and less urgent.

In the private sector - and among consumers - there is a greater energy. In February, one in four new cars sold in the UK was a battery electric vehicle. More solar panels were installed in the UK last year than ever before (more on that below).

In our next webinar, we’ll be using our 2026 fieldwork and trend analysis to answer the question; what is the state of sustainability? How important is it now to consumers and voters?

Photo courtesy of Related Stories

The webinar takes place on March 26th and is free.

To learn more about the webinar - and to register - punch the button below.

Storage Solutions

Every month I look at real-world examples of the commercial impact of our macro-trends.

President Trump’s unconventional and often startling approach to statesmanship has distracted world leaders (those who haven’t been incarcerated or have had their premierships cut short by the unwelcome arrival of an incoming missile). Existing priorities have had to be relocated to the back seat while the management challenge that is the 47th President of the United States is addressed. Consequently, even issues as pressing as climate change have received less attention than they are due. As the climate emergency slides towards the back of our collective mind, it’s perhaps reasonable to expect a recession in the green economy. Perhaps consumers, like their beleaguered governments, have different priorities now?

Some welcome perspective has been provided by an electrical wholesaler in St Helens. Speaking to a Trajectory operative, the wholesaler mentioned the recent acquisition of an additional industrial unit to house domestic batteries that can store the power generated by solar panels. The sudden demand for these batteries has led to a marked increase in our wholesaler’s turnover (they retail for between £1,200 and £6,000 each). This illuminating Merseyside aside sparked our interest (don’t worry, more puns are coming).

The Department for Energy Security and Net Zero collect data on battery installations largely through the Microgeneration Certification Scheme. Their data shows that consumer interest has amped up considerably. In 2023, there were 4,864 battery installations in the UK. A year later the number rose to 20,550. Last year MCS certified installers put in 40,717. In the same year, there were more than a quarter of a million solar panel installations (a record number). You might think that most of this increase has come from low-carbon generation technologies being designed into new-build homes. In fact, 71% of the installations were retrofitted into existing buildings.

It’s increasingly common for homeowners to add a battery when they install solar panels - about a third of consumers now do this.

The market for domestic batteries will be further charged by the government’s “biggest homes upgrade plan in British history.” Government policy is shifting from encouraging insulation towards the installation of solar panels and batteries. In January, the government announced £15 billion of support for lower-income families to install clean energy products into their homes. Additionally, the Future Homes and Buildings Standards plan will mandate the installation of solar panels and heat pumps into new builds.

As fossil fuel prices jump in the wake of ‘Operation Epic Fury,’* the green economy will receive a backhanded boost.

The momentum behind domestic battery installation is one manifestation of our (recently revised) Green Economy macro trend. The trend itself encompasses a variety of dynamics from legislative backsliding to shifts in economic focus and - at a consumer level - the early signals of significant changes in how we will live our lives.

Of course, the charge towards batteries has less to do with a desire to live sustainably and rather more to do with saving money in the long term - a central dynamic in the Green Economy.

*I would like to know who is in charge of naming military operations at the Pentagon. If that person has never seen a Steven Segal movie, I’d be surprised.

Subscribe to Trajectory

The world has become a more volatile place (just ask Fabien Galthié). For that reason, it’s vital to have an up-to-date understanding of what matters to consumers. Our monthly programme of quantitative research informs our subscription service and gives you a contemporaneous and reliable analysis of the consumer mood.

An annual subscription starts at the same price as 569 therms of wholesale natural gas. You know what I’m saying. I won’t labour the point.

Here are the options:

Now

An offline service that continually monitors the consumer pulse. Subscribers receive a monthly report, invitations to subscriber-only webinars and an analysis of consumer sentiment based upon our monthly fieldwork. £500 per year, per user.

Now & Next

The core, online, package. Access to monthly data, webinars, reports, articles and macro-trends. £3,200 per year per organisation (unlimited users).

Now & Next +

All of Now & Next plus offline humanity! We’re including analyst support in this package. There is also the ability to add your own questions to our monthly fieldwork with 1,500 nationally representative Britons. £7,500 per year per organisation (unlimited users).