Foreword

The monthly update from Trajectory: December 2025

No room at the inn for optimism

Our November fieldwork - which sampled 1,500 nationally representative Britons - found that optimism nudged marginally higher last month. It’s a gerbil-sized nudge though and the increase isn’t enough to move the three month rolling average which was unchanged for the period to November.

Overall, we remain just shy of the threshold of optimism.

The research was conducted before the Budget on the 26th, so we can’t yet tell you if the investment in the Lower Thames Crossing and the £20 million for the Peterborough sports quarter has lifted the mood of the nation.

As always, there is significance in the detail of the fieldwork. Those earning between £20k and £40k have experienced the greatest decline in optimism through 2025 as they continue to struggle with the cost of living. Their optimism has declined to such an extent that they now have a similar outlook to those on the lowest incomes. Those working and earning between £20k and £40k represent one fifth of all UK consumers - a sizeable and fairly cheesed-off constituency.

Last month, net confidence in the British economy fell like a fatalistic lemming. Confidence in the economy is now at its lowest point this year. Merry Christmas everyone.

The full detail and analysis from our fieldwork is available to our discerning subscribers. Our various subscription packages are listed at the bottom of this missive. Each makes for a thoughtful Christmas gift for your CMO.

The world in 2026

Our first webinar of the year is always our best attended. That’s because we use that hour to anticipate how the consumer mood may shift in the next twelve months. The recent mood of the nation has been one of Dickensian bleakness - we’ve spent just 4 of the last 48 months feeling optimistic about the future.

However, the bigger story is how polarised the UK has become. In 15 years of measuring consumer sentiment and public opinion, we’ve never seen the public more divided in their experiences of the present or their expectations of the future. (There’s a potent example of this further down this newsletter, BTW.)

Next year sees the Winter Olympics take place in Italy (Britain might not do that well but the catering will be great), the FIFA World Cup will take place in North America and the Commonwealth Games will be contested in Glasgow (where the standard of catering will undoubtably be similar to that of the Winter Olympics). There will be local elections in the UK and mid-term elections in the United States. An election to the Scottish parliament is scheduled for May 7th and that will serve as a test of the Reform Party’s appeal to a broad electorate. Scottish First Minister, John Swinney, is seeking to “confront” and “defeat” Nigel Farage - something that promises a pleasing level of Braveheart aggro.

Britain’s changing demography will be manifest next year as the retirement age starts to shuffle up to 67.

Make it your new year’s resolution to join us on January 29th at 09:00 am to consider the challenges - and opportunities - that another year will bring.

We already have a record number of registrations for the webinar but fear not - that queasy sensation of FOMO that you are feeling can dispelled by punching the button below.

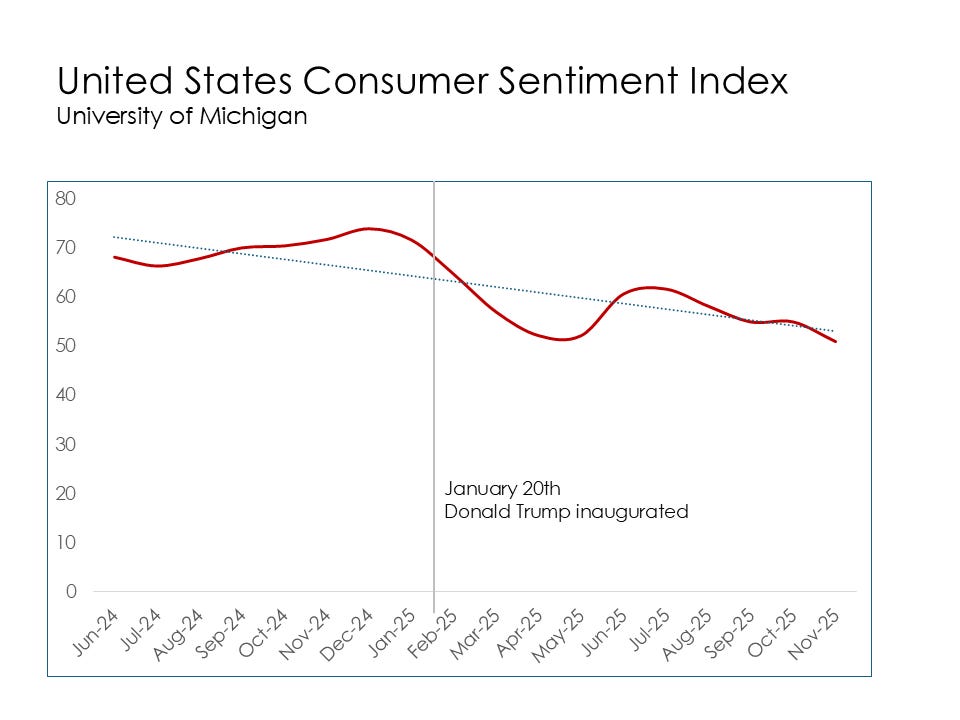

Stateslide: confidence trumped by concern

The grass is not always greener on the other side of the Atlantic.

I’m aware that this newsletter, thus far, has not been stuffed with festive cheer so, in an attempt to make you feel better (and with an eye to my Substack open rate), I thought I would contextualise optimism in the UK with sentiment in the USA. I can sense the researchers among you hyperventilating about methodologically dissimilar data comparisons, so I’ll state that the University of Michigan’s tracker only considers economic sentiment, whereas our Optimism Index is a broader measure that includes non-financial factors. Some would say ours is better.

Back in Michigan, Survey of Consumers Director, Joanne Hsu, states; “…consumers remain frustrated about the persistence of high prices and weakening incomes. This month, current personal finances and buying conditions for durables both plunged more than 10%, whereas expectations for the future improved modestly.”

Sustainable interest?

Every month I look at real world manifestations of the trends that we continually monitor.

Even when the conference centre went on fire, it was hard to see drama in the COP 30 summit in Brazil last month. This is not to say that progress wasn’t made but the absence of some world leaders reinforced the sense that climate change seems a less urgent challenge in 2025. President Trump describes the climate crisis as; “…the greatest con job ever perpetrated on the world.” Meanwhile, the Russians - never ones to put themselves out for others - said nyet to new roadmaps at COP 30. In Europe, regulators are back-tracking on emissions regulations. Globally, sustainability has slipped from news agendas.

How are consumer-citizens responding?

In higher-income countries, the proportion who see global climate change as a “major threat” to their country has declined. In 2022, 75% of Britons perceived climate change as a threat. Three years later the proportion has fallen back to 66%. The pattern is the same in Germany, France, Japan, South Korea and the United States according to Pew data.

In middle-income countries the trend is reversed - the citizens of Brazil, India and Turkey (among others) all now sense a greater threat from climate change than they did three years ago.

“The dinosaurs didn’t know what was coming, but we do” - Marina Silva, Minister of the Environment & Climate Change, Federative Republic of Brazil

Our own research corroborates the Pew work. Every month we ask consumers to state the three issues that are of greatest importance to them. Last month, climate change was the eleventh most mentioned item. A year ago, climate change was the ninth most important issue and the year before that the eighth - our interest in global warming is cooling.

Concern about climate is not universal and is closely aligned to political beliefs - an argument that we put forward in our Climate Contests trend. The trend states that; “There’s been a broad political consensus on Net Zero for a long time. As the costs mount and growth stutters, that consensus will break.”

Our data from last year shows that 89% of LibDem voters agree that; “climate change is an important issue and I am concerned about it.” Among Reform voters agreement is 52%.

The fracturing of the consensus on climate change has big implications for the world we’ll live in. Reform claim that scrapping net zero and related subsidies would save £30 billion a year, creating space for tax cuts or investment elsewhere. Responding to Reform’s 2024 manifesto, the RSPB stated; “We’re alarmed about the proposals in this manifesto to scrap net zero and the expansion plans for oil and gas. This would be in direct conflict with tackling the nature and climate emergencies and a rejection of the science and evidence.” The stakes are high.

Pew’s 2025 research shows a schism between left wing and right wing voters in most countries. In the United States, 20% of right-of-centre voters believe that global climate change is a major threat. Among left-of-centre voters agreement is 84% - a difference of 64 points. In Canada the difference between left and right is 40 points, in Germany it’s 34 points and in Spain 31 points.

Progress towards a more sustainable way of living will involve significant change and sacrifice. Thus far, the transition has been fairly inconsequential for consumers as businesses have covered a lot of the hard yards for them through providing some modest solutions - more efficient appliances, LED bulbs, the use of some recycled materials in the manufacture of products, more frugal petrol engines and boilers. What comes next is more difficult. Pew’s 2024 research shows that 23% of Americans expect to have to make “major sacrifices” in their lifetimes because of global climate change. Politically, net zero is a hard sell and it may force a realignment of the political parties here and abroad. It’s also entirely conceivable that opposition to net zero will intensify.

Season’s Greetings

It feels a bit early to wish you a Merry Christmas but, having said that, I acknowledge that the baubles and tinsel were staple-gunned to the walls of our local Harvester on September 18th. A Merry Christmas to our clients, subscribers, sister companies, suppliers and supporters. We’ll see you in the New Year.

Subscribe to Trajectory

The world has become a more volatile place (just ask Pete Hegseth). For that reason, it’s vital to have an up-to-date understanding of what matters to consumers. Our monthly programme of quantitative research informs our subscription service and gives you a contemporaneous and reliable analysis of the consumer mood.

An annual subscription starts at a fraction of the cost of the office Christmas party that you don’t particularly want to go to.

Here are the options:

Now

An offline service that continually monitors the consumer pulse. Subscribers receive a monthly report, invitations to subscriber-only webinars and an analysis of consumer sentiment based upon our monthly fieldwork. £500 per year, per user.

Now & Next

The core, online, package. Access to monthly data, webinars, reports, articles and macro-trends. £3,200 per year per organisation (unlimited users).

Now & Next +

All of Now & Next plus offline humanity! We’re including analyst support in this package. There is also the ability to add your own questions to our monthly fieldwork with 1,500 nationally representative Britons. £7,500 per year per organisation (unlimited users).

| A guest post by

|